AI Cycle Update

An extract from the full Investment Manager’s Report

The financial information set out below does not constitute the company's statutory accounts for the years ended 30 April 2026 or 30 April 2025 but is derived from those accounts. Statutory accounts for 2025 have been delivered to the registrar of companies, and those for 2026 will be delivered in due course. The auditor has reported on those accounts; their reports were (i) unqualified, (ii) did not include a reference to any matters to which the auditor drew attention by way of emphasis without qualifying their report and (iii) did not contain a statement under section 498 (2) or (3) of the Companies Act 2006.

The full Annual Report and Financial Statements for the Year Ending 30 April 2026 can be found here.

AI cycle update

Rapid adoption: users and tokens

AI adoption continues to significantly outpace historic trends seen with the PC, internet and smartphone. OpenAI recently announced it had reached 900 million weekly active users (WAU) with ambitions to grow to 2.6 billion WAU by 2030 while Google's Gemini AI surpassed 750 million monthly active users (MAU). User growth has helped drive AI usage, as measured by token growth which had been compounding at 4-5x annualised before appearing to accelerate to 9x annualised growth in January. In Altman's words, reasoning and agentic have taken AI into a "new phase where frontier AI moves from research into daily use at global scale".

Enterprise adoption begins

This is evident from Anthropic's revenue trajectory. Having ended 2024 at $1bn, Anthropic's annualised recurring revenue (ARR) reached a remarkable $14bn in February 2026, making it, at the time, the fastest-scaling business to business (B2B) company in the history of software. Since then, ARR exploded to $19bn in March, $30bn in April and – according to reports – $47bn in May. This is truly unprecedented; no company in history, to our knowledge, has ever reached $30bn of ARR within four years, let alone $47bn.

This revenue breakout reflects an inflection in enterprise AI adoption which had previously trailed consumer adoption due to early scepticism and inconsistent model performance. This is clearly no longer the case, with measurable productivity gains driving demonstrable RoI. Anthropic's analysis of Claude usage shows a median 84% time saving per conversation, concentrated in the 80-90% range for multi-step cognitive work. AI is collapsing the coordination cost of knowledge work, creating a self-reinforcing adoption loop: freed capacity justifies further investment in AI infrastructure and tooling.

As discussed in last year's Annual Report, agentic AI represents the architectural breakthrough that enables enterprise adoption because enterprises are built on repetitive, multi-step workflows that are too complex for a simple prompt but do not require human judgement at every step. Unlike chat, agentic AI can integrate with existing systems and complete work. By 2028, technology research firm Gartner expects 15% of day-to-day work decisions to be made autonomously by AI agents.

Rapid model progress

The emergence of agentic AI reflects the extraordinary pace of underlying model progress during 2025, a year that began with the DeepSeek R1 shock and ended with an unprecedented wave of frontier releases. AI systems evolved rapidly from conversational chatbots into reasoning-driven, multimodal agents able to operate across text, image, audio and video with expanding autonomy. Frontier closed-source models delivered major advances in reasoning, hallucination reduction, multimodal capability and million-token context windows, with leading systems achieving gold medal standard mathematical performance alongside near-human or superhuman coding ability.

Open-source models also advanced rapidly, led by a wave of Chinese releases, including DeepSeek R1, that brought frontier-level performance to dramatically lower price points. Momentum accelerated further in early 2026 as systems such as Claude Code and open-source autonomous agents demonstrated how quickly AI is evolving from a passive assistant into a practical digital worker, while models such as Claude Mythos Preview hinted at levels of reasoning, autonomy and technical sophistication previously associated only with highly specialised human experts.

Ben Rogoff

Partner, Technology

Alastair Unwin

Partner, Deputy Fund Manager

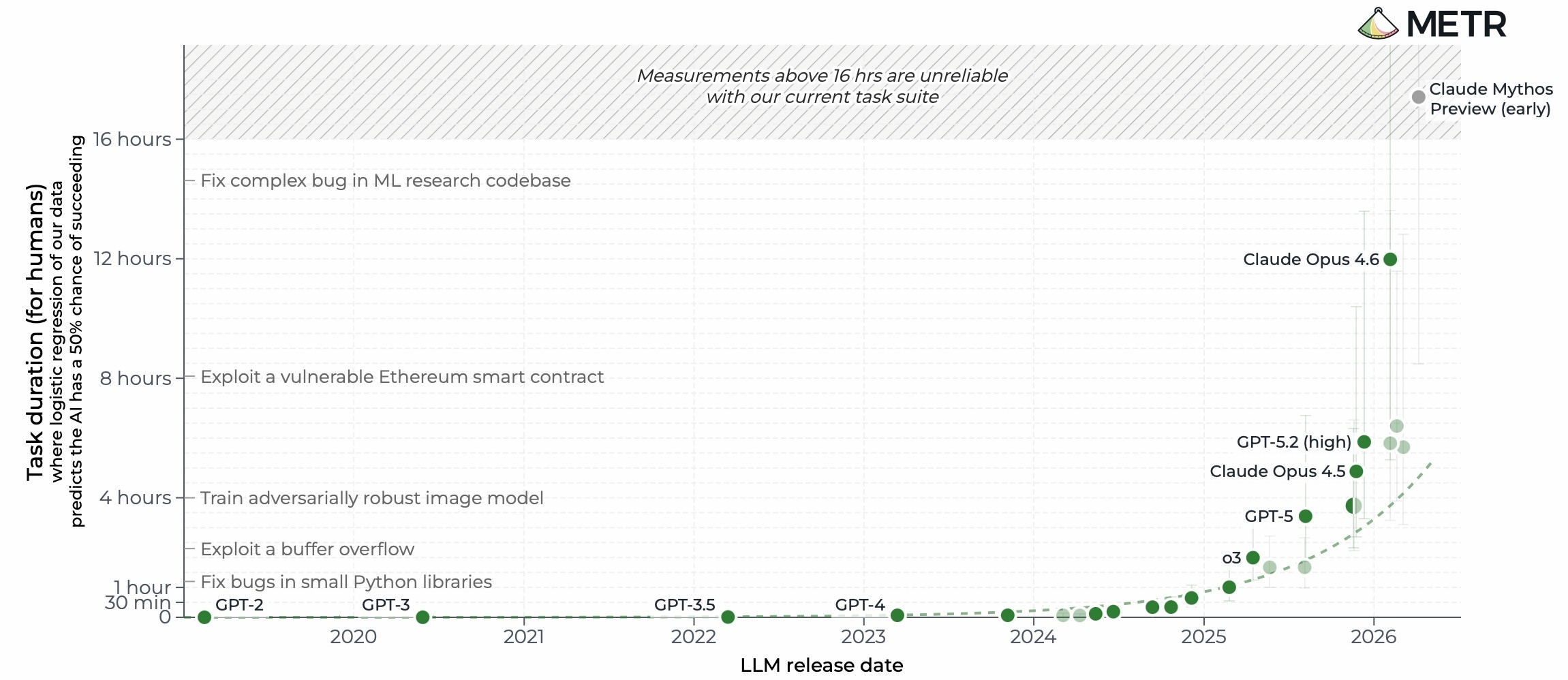

Task-completion time horizon

As previously discussed, agentic AI introduces the prospect of non-human scaling in cognitive labour. Accordingly, one of the most important frontier AI benchmarks today is the duration and complexity of tasks a system can reliably complete autonomously. The so-called task-completion time horizon measures the length of a task – based on expert human completion time – that an AI agent can successfully complete at a given level of reliability. A 50% time horizon represents the task duration at which an agent succeeds half the time. Until recently, the duration of tasks AI systems could complete was doubling roughly every seven months – already an extraordinary rate of progress – but since 2024 this pace has accelerated to closer to every four months. At this threshold, ChatGPT (2022) could autonomously perform tasks requiring less than a minute of human expert effort; GPT-5.2 (2025) could manage tasks exceeding six hours; Anthropic's Opus 4.6 (2026) – the model underpinning Claude Code – has reportedly extended this horizon to 14.5 hours.

The coding breakthrough

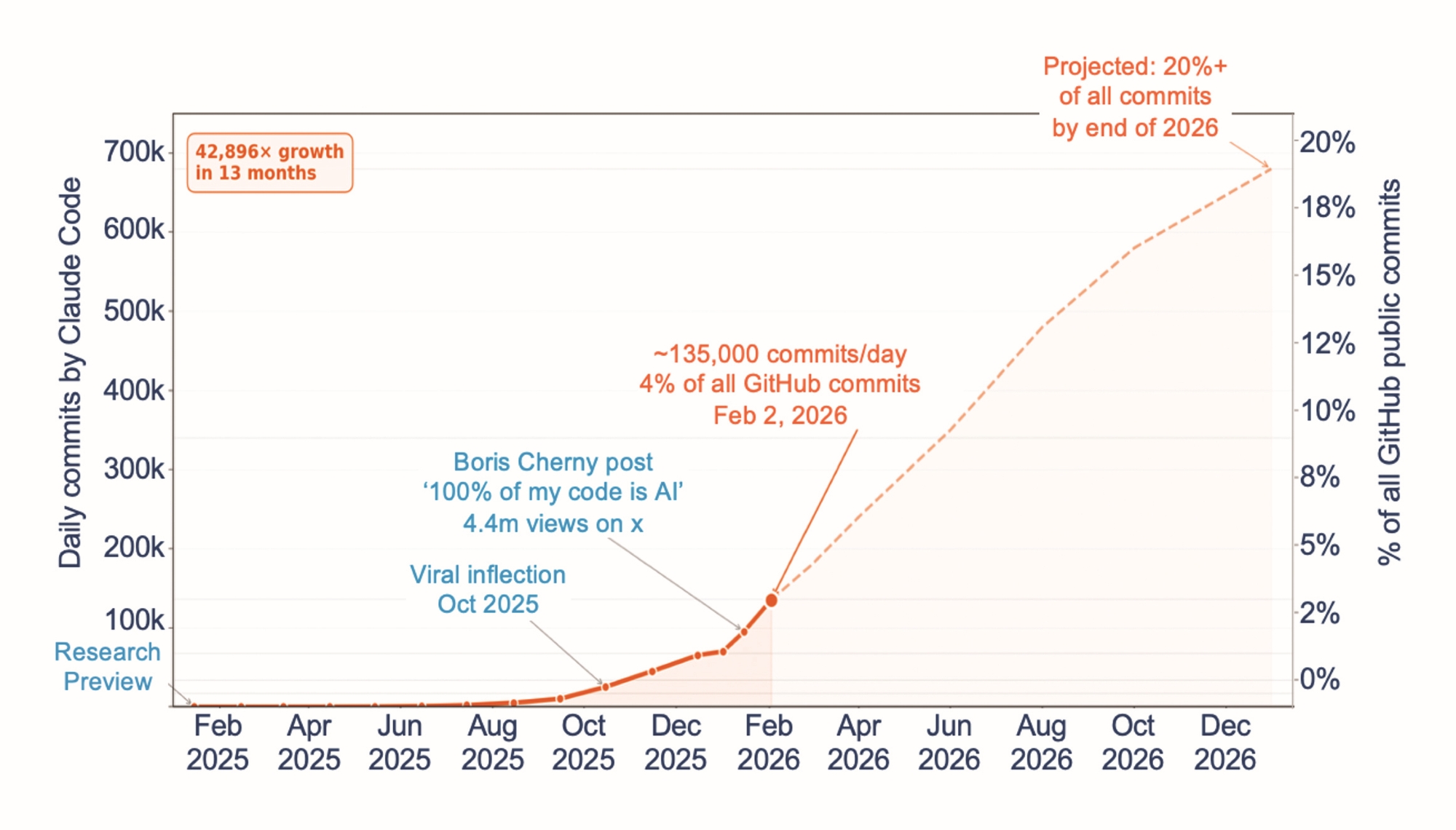

This remarkable progress has appeared first in coding. In early 2025, Anthropic launched Claude Code, a command-line coding agent able to autonomously navigate codebases, write and edit code, run tests and commit changes with minimal human oversight. By September, Claude Code had reached $1bn ARR and, in December, Boris Cherny – its creator – stated that 100% of his commits (unit of code) were written by Claude + Opus 4.5. Daily GitHub commits attributed to Claude Code rose to 4% of all public GitHub commits, an extraordinary 43,000× increase in roughly 13 months. A commit is not code itself, but rather a snapshot of changes to a repository and one of the few observable, standardised time-series signals for software production.

While this may appear to be 'just' faster coding, it is better understood as non-human scaling and helps explain why AI has entered a more disruptive phase. The release of Cowork in January extended Claude Code to non-technical users. More importantly, as AI shifts from tool to autonomous worker, RoI follows. Although just one example, Anthropic's revenue trajectory also undermines earlier claims that AI revenues were insufficient to justify current levels of capex. Nor should it surprise us that systems capable of autonomously completing multi-hour tasks possess far greater economic value than those limited to minutes. Just as skyscrapers transformed the value of land by conquering vertical space (and thus it became economic to replace early skyscrapers with taller structures on the same site very quickly), so conquering cognitive depth is transforming the value of AI.

Source: Claude generated from Semianalysis.

Code as a reasoning substrate

The coding breakthrough also matters because code has become part of the reasoning process itself, rather than merely an output. Frontier models increasingly use code to externalise state, memory, iteration and precision into deterministic systems better suited to those tasks. A useful analogy is using AI to calculate a tax return. Previously, the LLM had to perform the entire calculation within token space: interpreting the tax code, applying thresholds, carrying figures forward and holding all dependencies simultaneously in memory, with small reasoning errors compounding along the way. Today, the model is not doing the tax return directly – it writes the system that does the tax return. The reasoning and synthesis still come from the model, but calculation, state management and iteration are offloaded into Python. By externalising or offloading cognition, a probabilistic LLM produces deterministic, repeatable output.

Capex and the AI race

In his 2020 shareholder letter, CEO Jeff Bezos quantified the value of Amazon Prime in terms of time saved. He estimated Prime saved members more than 75 hours annually versus physical store trips, valuing that at roughly $630 per member against a subscription price of $119. Time is also a useful lens through which to view AI progress, given that many of the key benchmarks are denominated in time, including autonomous task duration and the acceleration of human work. Applying this framework to the developed-world knowledge wage bill ($23trn), assuming half is addressable by current AI and using Anthropic's estimate of 80% time savings, generates $9-10trn in equivalent labour value. Applying an Amazon-style 16% capture rate suggests a potential AI revenue opportunity more than $1trn today – and this captures only the current visible market opportunity. In 1998, the internet addressable market was framed as a share of the existing $500bn global advertising market; today, e-commerce, digital advertising and video streaming together exceed $7trn. AI may unlock similarly large invisible markets that are difficult to frame today.

Looks like convergence…

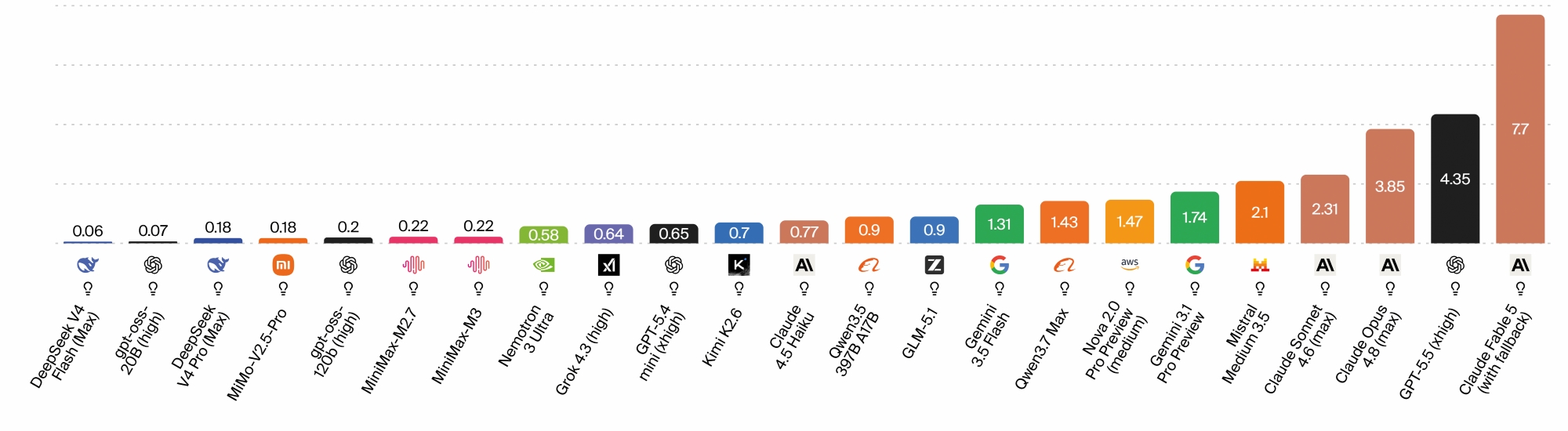

From a distance, AI models appear to be converging. On benchmarks such as MMLU (massive multitask language understanding), leading systems now cluster above 85%, while open-source models often launch at 90% of frontier performance and close much of the remaining gap within months. Chinese models are believed to trail US frontier labs by less than a year, while architectures themselves are converging around mixture-of-experts (MoE) designs. DeepSeek's release of R1 in January 2025 crystallised the commoditisation narrative: it matched OpenAI's o1 on many benchmarks while charging just $2.19 per million output tokens versus o1's $60. Today, open-weight models such as Qwen3 and Meta AI's Llama 4 offer near-frontier capability at close to zero marginal cost.

This convergence, however, is largely a mirage. Static benchmarks obscure widening gaps in economically valuable capabilities. On SWE-bench Pro – a demanding real-world coding benchmark – frontier models such as Claude Opus and GPT-5 solve more than 20% of tasks, while open-weight Qwen3 32B achieves just 3.4%. Frontier systems also reason differently, exhibit distinct strengths and produce materially different outputs. Unlike compute or storage, cognition is not fungible. That helps explain why closed-source models still account for roughly 80% of token usage and 96% of industry revenue despite costing, on average, eight times more per token than open alternatives.

Front-runners breaking away from the pack

Today, the frontier appears increasingly concentrated around three companies: Anthropic, OpenAI and Google DeepMind. Everyone else is either a tier below or reliant on one of these for their intelligence layer. That these three companies' models are clustered or trading positions in benchmarks is not evidence of commoditisation. It means that only they are today able to compete at this level. Meta is spending enormous sums, but Llama is today a strong open-weight model, not a frontier one. Amazon Nova competes on cost, not capability. Smaller and open-weight models can match frontier performance on isolated tasks but degrade sharply when each step depends on the previous one.

This heightened level of intensity is evident in soaring capex budgets, high-profile talent wars and faster model iteration. In less than a month during late 2025, four frontier labs launched their most powerful models: Grok 4.1, Gemini 3, Claude Opus 4.5 and GPT-5.2. Since then, the pace has only accelerated. The leading labs are locked in a pace that is self-reinforcing: every capability jump resets the field and compresses the interval to the next one, with perceived leadership shifting with each new model breakthrough. Huge differences in token prices for the most capable models indicate the market reality of the returns to frontier intelligence.

The AI race is one the smartest companies know they cannot afford to lose. Now that agents are viable, it should be clear that the LLM increasingly resembles the operating system of the agentic world – the layer that interprets intent and orchestrates execution. Any company without a frontier model is building on someone else's operating system, exposed to margin compression, feature absorption and – in an age of abundant code – rapid obsolescence.

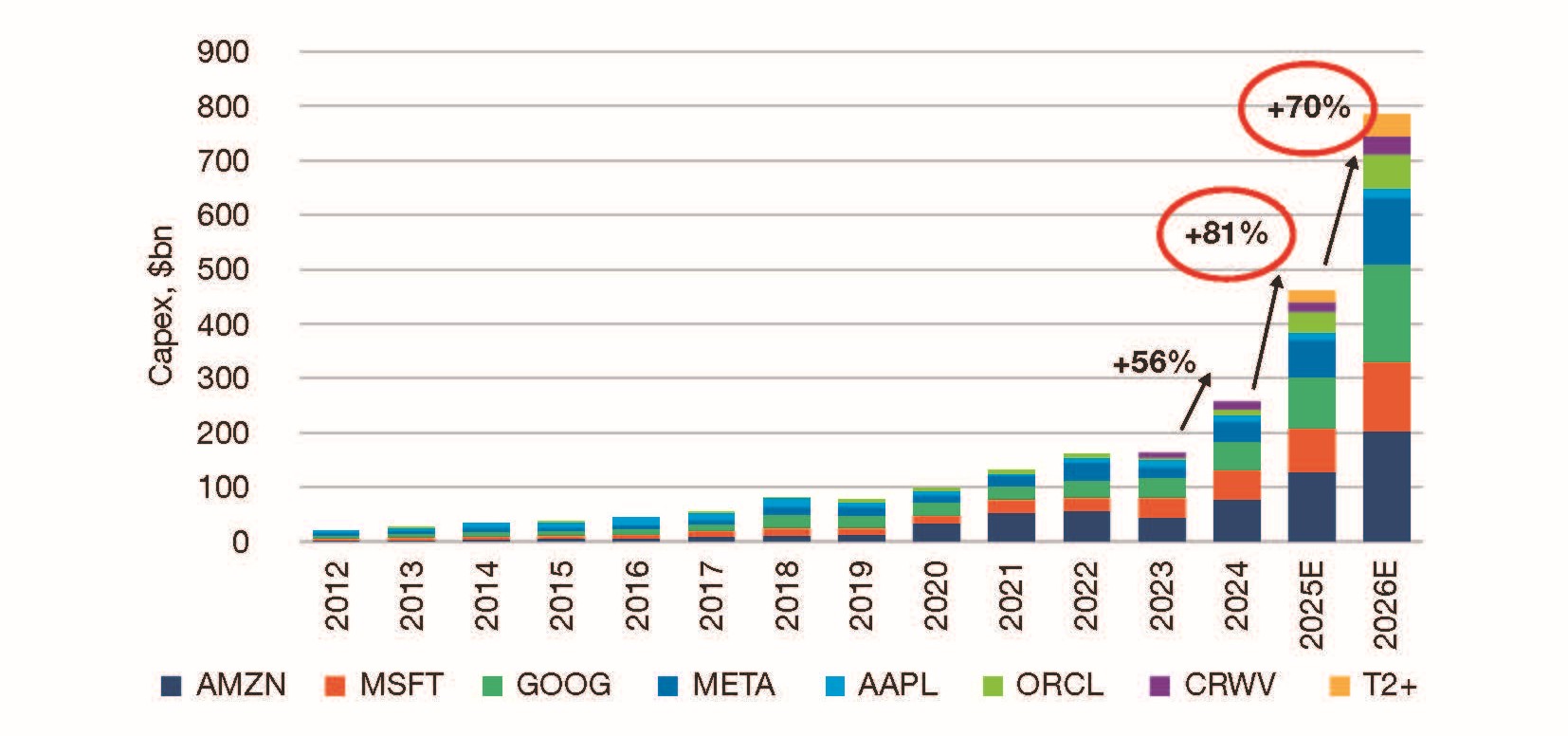

That is why capex budgets can be both historic and entirely rational. Following an extraordinary 2025, AI capex is now expected to approach $800bn (+70% y/y) this year. Amazon, Alphabet, Meta, Microsoft and Oracle alone plan to spend as much as $690bn (+60% y/y) from already historic 2025 levels, while China is also scaling rapidly with $125bn spent on AI capex last year. Between the two blocs, global AI infrastructure spending is approaching $1trn annually. The conviction behind it is simple: the industry is supply constrained, AI workloads will consume every available unit of compute capacity and the penalty for underbuilding is existential. The cost of staying in the race is also compounding, with each generation of frontier model requiring roughly an order of magnitude more compute alongside a rapidly growing inference burden – inference workloads already consume over 55% of AI-optimised infrastructure spending in 2026, up from a third in 2023.

Who could leave the table?

While each participant in the AI race has their own motivations, history suggests that as the ante rises the number of players thins out. The xAI/SpaceX merger – while framed around the vision of orbital data centres – may have been a strategy to ensure that xAI had access to the capital required to stay in the AI race. Oracle plans to raise $45-50bn in debt and equity this year having spent like a hyperscaler without the balance sheet of one. At the same time, others could yet join the game: Microsoft could enter the frontier race having relied on OpenAI for model access, with Microsoft AI CEO Mustafa Suleyman explicit in wanting Microsoft models "at the absolute frontier". Apple also remains a wildcard, with $130bn in cash and its CEO due to step down in September. As for the AI labs, both continue to raise capital relatively easily: in February, Anthropic closed a $30bn funding round while OpenAI raised $110bn, the largest private financing in history.

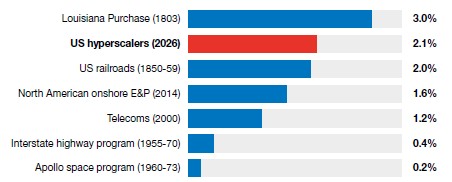

Source: Companies World Bank, Wall Street Journal and S&P Global

Disruption, accelerated

In today's digital economy, attention scarcity is monetised at every layer. Instead of the so-called 'long tail', we created vast new digital gatekeepers that helped humans make informed choices from an almost infinite range of alternatives. Data exploded 32-fold in a decade, helping to defend, optimise and scale the digital winners into the natural monopolies that many are today. However, AI represents three principal risks to these profit pools: abundant code, non-human actors, and a natural language interface.

Abundant code: The modern digital economy rests on roughly 2.8 trillion lines of code written over the past two decades, of which perhaps one trillion lines remain actively maintained. In 2010, the world produced around 33 billion lines of new or modified code per year; by 2024, AI coding assistants were producing 256 billion lines, with 41% of all new code now AI-generated. Today, tools like Claude Code and OpenAI's Codex can independently write software, improve existing code and even submit completed updates with minimal human involvement. The cost per line of code has followed: from $7-15 pre-AI, to $2-4 with assistants, to sub-$2 with agentic systems – and falling, as token prices decline at roughly 90% per year. The digital platforms were built when code was scarce and expensive. Today, the marginal cost of code is converging on zero.

Non-human actors: Pre-AI digital profit pools were earned by solving a real problem: helping humans navigate infinite choice and monetising the time/value trade-off at the heart of every digital interaction. 'Time is money' has underpinned two centuries of economic logic, and the entire margin structure of the digital platforms, but agents have infinite time. A human will pay for a shortcut; an agent will simply do the work. That distinction matters because the moats that took a decade to build – network effects; data flywheels; switching costs – were durable in a world where iteration was slow, learning was expensive and time was scarce. Agents face none of these constraints. They operate on a different efficient frontier, optimising for compute costs, not time.

Natural language interface: Every previous interface revolution made software easier to use, e.g. command line to graphical user interface to touchscreen. Each also diminished the value of incumbency, breaking habits and rendering previous workflows obsolete. However, the LLM is significantly more disruptive. It responds to intent, not instruction, unbundling the human operator from the application itself and making software redundant as an interface layer.

Abundant code lowers the barriers to entry. Non-human actors erode the willingness to pay. The natural language interface unbundles the user from the application. Together, they represent a profound challenge to many digital incumbents.

In information services, AI can approximate datasets that were previously valuable because they were hard to assemble rather than fundamentally secret. The moat was never the data, but the human labour required to collect, synthesise and curate it. AI collapses that labour by 80-90%. In software, three moats look challenged – data trapped inside the application, workflow lock-in from learning the user interface (UI) and integration complexity between systems. In an AI-first world, the application becomes a backend service that the LLM orchestrates, not a product that a human operates.

Advertising – worth $1trn by 2028 – also appears AI-exposed. Performance advertising is today built on attention scarcity with platforms monetising the space between intent and action. Agentic commerce may also reshape e-commerce – Morgan Stanley estimates agentic gross merchandise value could reach $190bn in a base case and $385bn in a bull case by 2030, implying 10-20% of US e-commerce. Content is likely to be highly disrupted too, as high-quality AI-assisted video content continues to improve and become significantly cheaper. Last year, UK creative agency headcount fell 14% year-on-year, the steepest decline since records began. Within five years, McKinsey estimates $60bn of content revenue could be redistributed.

These areas potentially at risk from disruption are not exhaustive. Any business whose competitive advantage exists purely as executable code sits on a different risk curve. Disruption risk extends well beyond code; agentic AI systematically attacks confusion, inertia and opacity – three of the most profitable features of the consumer economy today.

Technology risks

As we have previously outlined, the principal technology risk to the AI cycle and our portfolio is that the pace of model progress, adoption or monetisation fails to justify the historic level of infrastructure investment currently underway. Much depends on continued confidence in scaling laws; however, these are empirically observed rather than theoretically derived and there is no fundamental reason they must continue indefinitely. Data scarcity, diminishing returns from pre-training or an architectural breakthrough that invalidates the current paradigm could each flatten the current trajectory.

Regulation adds a further layer of uncertainty. The EU AI Act is now in force, US state-level legislation is proliferating and unresolved copyright litigation could yet establish precedents that materially alter the economics of frontier model development. More broadly, sufficiently rapid advances in frontier capability could provoke direct state intervention, including licensing regimes, restrictions on model releases or greater government oversight of frontier labs, any of which could alter how AI value accrues across the ecosystem.

There are also risks associated with the financing of this investment cycle. While we are broadly comfortable with the increasingly interconnected capital flows between industry participants – which we view as a form of vertical integration in a stack no single company fully controls – they nevertheless create system-level fragility. The structure depends on AI revenues materialising on a timeline compatible with capital deployment. JP Morgan estimates cumulative AI capex requirements of $5.3trn through 2030, with a $1.4trn financing shortfall emerging even after hyperscaler cashflows, investment-grade bond issuance, securitisation and leveraged finance are fully utilised. Private credit is expected to bridge much of that gap, although recent indicators have been mixed.

Hyperscaler balance sheets are also becoming materially more capital intensive: the roughly $2trn of AI assets planned by the five largest hyperscalers could imply annual depreciation expense of $400bn by 2030, greater than their combined 2025 profits. Except for Alphabet, none of the hyperscalers currently controls a leading frontier model, meaning current spending increasingly resembles a Red Queen dynamic in which participants must keep running simply to maintain competitive positioning.

The AI cycle is also exposed to a range of infrastructure and supply-chain risks. AI demand remains constrained by the availability of power, networking, advanced semiconductors, memory, packaging and data centre capacity, leaving the industry vulnerable to bottlenecks, delays and cost inflation. Power may prove the most underappreciated constraint. Training and serving frontier models increasingly requires gigawatt-scale infrastructure. US grid interconnection queues are measured in years, and new gas turbine delivery times now extend to 5-7 years.

Geopolitical tensions represent a further material risk, particularly around Taiwan and US/China relations, given Taiwan's dominant role in advanced semiconductor manufacturing and China's importance across both supply and demand. Export controls, tariff escalation, restrictions on rare earth minerals or disruption to semiconductor supply chains could materially affect AI infrastructure deployment, sector valuations and, by extension, our 'AI maximalist' portfolio positioning.

Current Base Management Fee Arrangement:

effective 1 May 2022

| 0.80% | £0 - £2bn |

| 0.70% | £2bn - £3.5bn |

| 0.60% | over £3.5bn |

Base Management Fee Arrangement:

to 30 April 2022

| 1% | Up to £800m |

| 0.85% | £800m - £1.6bn |

| 0.80% | £1.6bn - £2.00bn |

| 0.70% | over £2.0bn |

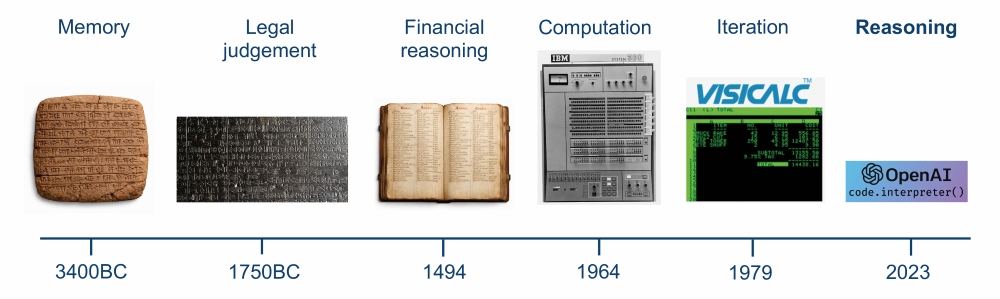

Our AI bull case: cognitive abundance

The industry's most prominent figures have made predictions that would once have sounded absurd. Anthropic CEO Dario Amodei has argued that AI-enabled biology and medicine may condense 50-100 years of human progress into 5-10. In his recent essay The Adolescence of Technology, he defines "powerful AI" as a system smarter than a Nobel Prize winner across most relevant fields, able to carry out tasks autonomously, with enough compute to run millions of instances of itself – a "country of geniuses in a data centre" – and in 2024 suggested this could be as little as 1-2 years away. DeepMind CEO Demis Hassabis has spoken of drug discovery becoming a thousand times more efficient while Sam Altman has suggested AI could compress a decade of scientific progress into a single year. While these claims echo Ray Kurzweil's long-standing view that technological progress compounds far faster than human intuition allows, they also assume cognitive abundance: AI cheap and continuous enough to put billions of minds to work in parallel.

There is a precedent for abundance turning a known resource from input to substrate. By 1901, oil - refined into kerosene - lit the world's lamps. While it had already made Standard Oil one of the most valuable companies on earth, everything that moved the economy - the trains, the ships, the factories - ran on coal. For the same heat, oil cost four times as much.

Spindletop changed that. On 10 January 1901, the Lucas gusher on Spindletop - a salt-dome hill in Texas - blew oil 150 feet into the air at 100,000 barrels a day, more than every other US well combined at the time. The price collapsed to three cents a barrel – for a time, cheaper than water - and oil became something to burn rather than merely to light. Within the year, railroads and steamships began converting from coal, and within a decade a lamp fuel had become the substrate of the industrial world.

Today, intelligence is the kerosene of the modern economy. The breakthrough in task duration may be AI's Spindletop. If so, the claims of Altman and his peers are not so fantastical — and the question becomes not whether to dismiss them, but what would need to be true for them to be even directionally right.

The easiest way to underestimate AI is to mistake the current interface for the underlying capability. ChatGPT is to AI what the telegraph was to electricity – a narrow early application of a far more significant general-purpose technology. We ask AI to slot into workflows designed around scarce, expensive human attention, just as early factories bolted electric motors onto steam-era layouts. The deeper opportunity is to redesign around abundant cognition from the outset. The binding constraint today is not cost – at current token prices, even an Edison-scale invention is computationally cheap – but continuity: reliable, persistent, reality-linked cognition over long durations. That bottleneck does not look permanent. Context windows are expanding, memory architectures improving, agents are learning to coordinate tools and sub-tasks over extended horizons.

The deeper implication is institutional. No single human mind could hold the Apollo space programme end-to-end; tens of thousands of people each understood a fragment – heat shields, guidance software, orbital mechanics etc made compatible through shared standards, hierarchies and records. Bureaucracy, in Weber's sense, was itself a form of externalised rationality: the historical solution to cognitive scarcity was to break problems into human-sized pieces and build institutions to coordinate them. AI does not merely substitute for the specialists working on those fragments. As context, memory and agency scale, it begins to encroach on the institution's deeper function – the coordinating intelligence that keeps the whole problem in view.

Current Base Management Fee Arrangement:

effective 1 May 2022

| 0.80% | £0 - £2bn |

| 0.70% | £2bn - £3.5bn |

| 0.60% | over £3.5bn |

Base Management Fee Arrangement:

to 30 April 2022

| 1% | Up to £800m |

| 0.85% | £800m - £1.6bn |

| 0.80% | £1.6bn - £2.00bn |

| 0.70% | over £2.0bn |

The richest problems – protein folding; materials discovery; climate modelling; drug design – sit at the intersection of domains no individual human can hold simultaneously in their mind. Specialisation was the workaround; the polymath was the rare exception. Abundant cognition collapses that constraint, allowing combinatorial search across domains that humans could only ever explore sequentially. The prize is problem-solving systems whose logic we can observe in operation without ever fully containing it in thought. Asked why LLMs work at all, Noam Shazeer, one of the architects of the transformer, replied: "My best guess is divine benevolence. Nobody really understands what's going on."

Oil transformed existing markets – ships and railways – but its real consequence lay elsewhere. Oil was a liquid; the change of state opened markets a solid could never reach: the automobile, and behind it the aeroplane, the highway, the petrochemical economy – none of which was visible from the boiler room. So it is likely to prove with cognition. The cheaper, faster analysis available today is remarkable but still only substitution. The transformation lies in the markets that could not previously exist at all: the space of things worth trying that we have never been able to afford to try.

This is why the 'low-hanging fruit has been picked' objection collapses. The sequence space for a modestly sized protein is 10²⁶⁰; nature has produced perhaps 10¹³ across all species. The space of drug-like molecules is estimated at 10⁶⁰; chemistry has synthesised roughly 10⁸. DeepMind's GNoME work expanded the catalogue of stable inorganic crystals from 20,000 to 421,000 in a single study – centuries of experimental progress in one pass and still a negligible fraction of the wider design space. The fruit was never too high. We have barely entered the orchard.